Q: I have been long debating variable or fixed rates for my existing portfolio. I have 3 properties and I am looking into breaking the current mortgages to either take a variable rate or a lower fixed rate. Which in your opinion is the better option?

A: Ahh, the dreaded variable vs fixed dilemma. This is a really tough question to answer without first analysing your portfolio and learning more about your income, your assets, how leveraged your portfolio is, what the cashflow looks like currently (and what it will look like in the future) and more. So realistically, this is a discussion we should have once I have more information. However, I will try to generalize the question as much as possible so that others who are thinking of the same question may be able to better analyse this.

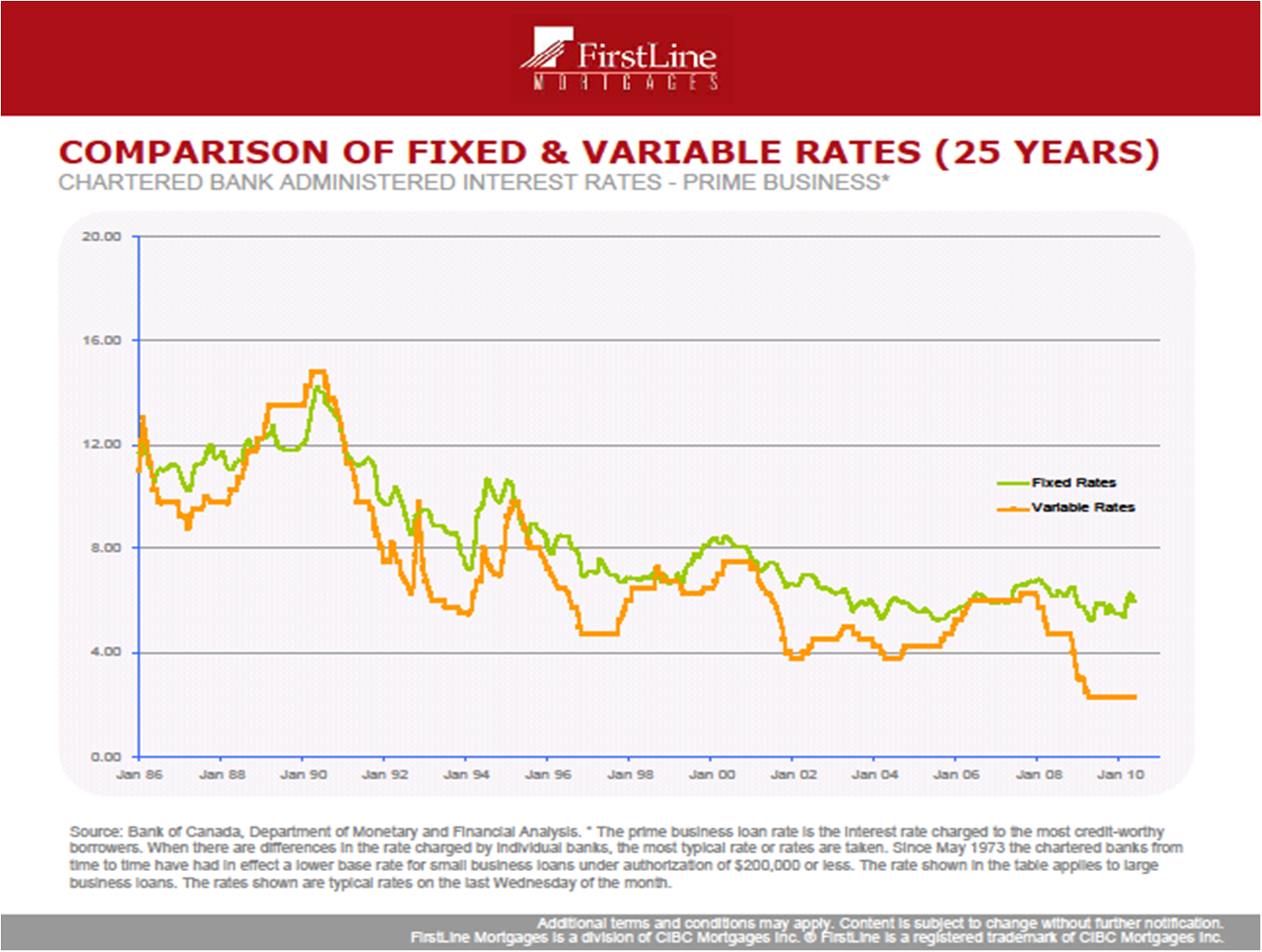

Reasons you may consider going with a fixed rate:

– The cashflow will still be positive with a 5 or even 10 year rate, which will give you security for the next 5-10 years. Many clients recently have been looking hard and long at a 10 year rate (5.05% as of Jan 4, 2011) because their property cashflows positively at 5.05% and Canadian home prices historically are always higher over a 10 year period, no matter what recessionary period that may be draped over. More specifically, in Vancouver, we see the same (http://cuer.sauder.ubc.ca/cma/data/ResidentialRealEstate/HousingPrices/housing-pri-vancouver.pdf). So if you can almost guarantee your cashflow AND appreciation doesn’t that make sense?

– You simply cannot afford the payments if rates go higher. This is especially important if you have a large exposure to variable rates (multiple properties) and don’t have the income or assets to absorb large increases in the prime rate. I usually like to determine what the payments would be at a Prime rate of 6%, where we have seen prime hang around in a balanced economy for roughly the past 10 years (inflation 2-3%).

– You find yourself watching and worrying about the stock and bond markets too much, and want to get some sleep at night!

– The average fixed rates over the last 25 years have been nearly 9%, and you are under the impression that a high inflationary period is soon to follow and that fixing your rates is the way to go.

Reasons you may consider going with a variable rate:

– If you are looking at flipping or owning the property for a short period of time. The penalties are likely to be lower (3 month interest penalty only, IRD or Interest Rate Differential penalties do not apply to variable rates) as variable rates are likely to be lower short term, a 3 month interest penalty will be lower with a variable rate short term.

– If you want flexibility. Remember that you can lock in to a fixed rate at any time, but make sure you have good lock in privileges. Many major banks do not guarantee their lowest rates or a specific discount when locking in, whereas many brokerage lenders who do not have posted rates simply offer their lowest possible rate when locking in.

– If you need short term cashflow. In some instances you may have no choice but to go short and hope that your cashflow improves in the next few years.

– If you can afford the payments if the prime rate rises substantially. This may be via personal income or other liquid assets. Also, if the property cashflows positively even at high rates it may make sense to go variable.

– If you are paying your mortgage off very aggresively. By paying down significant amounts of the principal now, you will lower the effect of higher interest rates because by the time the rates are higher, so is your mortgage balance.

– You believe that because historically variable rates have outperformed fixed rates that it will continue to do so.

At the end of the day, many economists are predicting that over 5 years the interest paid on a variable vs a fixed mortgage will be close. Most of the time this decision is a personal decision and sometimes it’s simply what helps you sleep at night.

Talk to me if you would like to get a better handle on making this decision at any time, 778-373-5441 or kgreen@mortgagealliance.com

Be the first to post a comment.